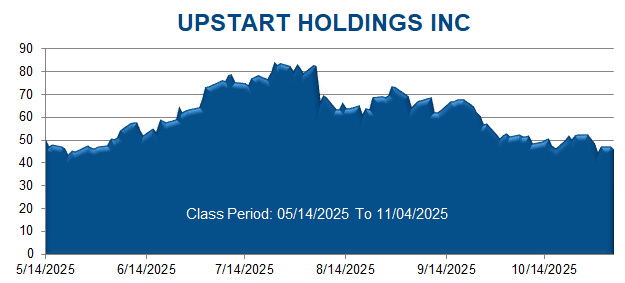

A securities class action has been filed against Upstart Holdings, Inc. (UPST) on behalf of a class consisting of all persons and entities other than Defendants that purchased or otherwise acquired Upstart securities between May 14, 2025 through November 4, 2025. This case has been filed in the USDC – NDCA.

Upstart, together with its subsidiaries, operates a cloud-based artificial intelligence (“AI”) lending platform in the U.S. Its platform includes unsecured personal loans, small dollar loans, auto refinance, auto retail loans, auto secured personal loans, and home equity lines of credit.

The complaint alleges that throughout the Class Period, Defendants made materially false and misleading statements regarding the Company’s business, operations, and prospects. Specifically, Defendants made false and/or misleading statements and/or failed to disclose that: (i) Model 22 frequently overreacted to negative macroeconomic signals in performing its risk-separation processes; (ii) accordingly, Model 22’s overall accuracy and propensity to increase loan approval rates was overstated; (iii) Model 22’s overly conservative assessment of credit and macroeconomic conditions was having a significant negative impact on Upstart’s revenue results, rendering the Company’s previously issued FY 2025 revenue guidance unreliable and/or unrealistic; and (iv) as a result, Defendants’ public statements were materially false and misleading at all relevant times.

The truth began to emerge on November 4, 2025, when Upstart issued a press release reporting its financial results for the third quarter (“Q3”) of 2025. Upstart reported, inter alia, Q3 2025 revenue of $277 million, missing its previously issued Q3 2025 revenue guidance of approximately $280 million, as well as consensus estimates by $2.62 million. Upstart also reported that it expected to generate revenue of only $288 million in the fourth quarter (“Q4”) of 2025, significantly below consensus estimates of $303.7 million. Further, Upstart negatively revised its FY 2025 revenue guidance to approximately $1.035 billion, versus the $1.06 billion consensus estimate and its prior guidance of approximately $1.055 billion, as well as its expected FY 2025 revenue from fees, which it reduced to approximately $946 million from its prior outlook of approximately $990 million.

The same day, during a related earnings call, Defendants blamed Upstart’s disappointing results on Model 22, which they revealed had “overreact[ed]” to macroeconomic signals in the quarter, reducing borrower approvals and conversion rates. Defendants also acknowledged that they had “knowingly” calibrated their AI model to be “more conservative on the credit side in earlier parts of the quarter”, and that the negative impacts of Model 22’s “overresponsive[ness]” to macroeconomic signals in the quarter would continue to negatively impact revenues in Q4 2025, resulting in Upstart’s negatively revised FY 2025 financial guidance.

Following these disclosures, Upstart’s stock price fell $4.49 per share, or 9.71%, to close at $41.75 per share on November 5, 2025.